Published by Don Hagan

First and foremost, Robo-Advisors are not advisors at all. This is once again another example of a Wall Street marketing ruse designed to mislead the public into believing they will receive individual attention, help when they need it and optimal risk-managed portfolio design. Robo-Advisors are really “Robo-Portfolios” based on software programs that have been around for decades. The software is based on two principals: 1) Buy and Hold and 2) Modern Portfolio Theory – which isn’t quite modern since it was first developed in 1952 by Harry Markowitz.

The first principal, Buy-and-Hold, speaks for itself. No matter what the market environment, no matter how bad the performance, no matter how dire the situation, one buys and never sells. To understand Buy-and-Hold, one needs simply to reflect on the performance of the S&P 500 from 1966 to 1982. The market went nowhere for 16 years. You may be thinking, “That was a long time ago, that wouldn’t happen now.” Well, take a look at the S&P 500’s performance from March 24, 2000 through March 3, 2013. The S&P 500 went nowhere for almost 13 years.

A Robo-Advisor’s portfolio allocation makes no distinction between if the market is overvalued or undervalued. A Robo-Advisor doesn’t take into account market risks, such as whether interest rates are rising, oil prices are plummeting or Lehman is going bankrupt. A Robo-Portfolio holds all of the stocks in an index, rather than having a selection criteria designed to focus on the best and weed out the rest.

The second principal underlying many Robo-Portfolios is based on Modern Portfolio Theory (MPT) and the Capital Asset Pricing Model, sometimes referred to as “CAPM.” Here are some of the important elements relating to the definition of MPT and CAPM, according to Wikipedia:

- “MPT is a mathematical formulation of the concept of diversification in investing, with the aim of selecting a collection of investment assets that has collectively lower risk than any individual asset. This is possible, intuitively speaking, because different types of assets often change in value in opposite ways. For example, to the extent prices in the stock market move differently from prices in the bond market, a collection of both types of assets can in theory face lower overall risk than either individually.”

In other words, the goal of diversification in MPT is to buy investments that go down when stocks go up, so that returns are more evenly distributed. Yes, you read that correctly. An investor subscribing to the MPT scenario would intentionally purchase something that goes down when stocks go up. Therefore, an investor most certainly will have to own stocks when stocks are in the midst of a steep decline. In the end, the hope is that if stocks go down, then the asset that was bought to even out the returns will go up and offset some of the decline. Unfortunately, it doesn’t work that way.

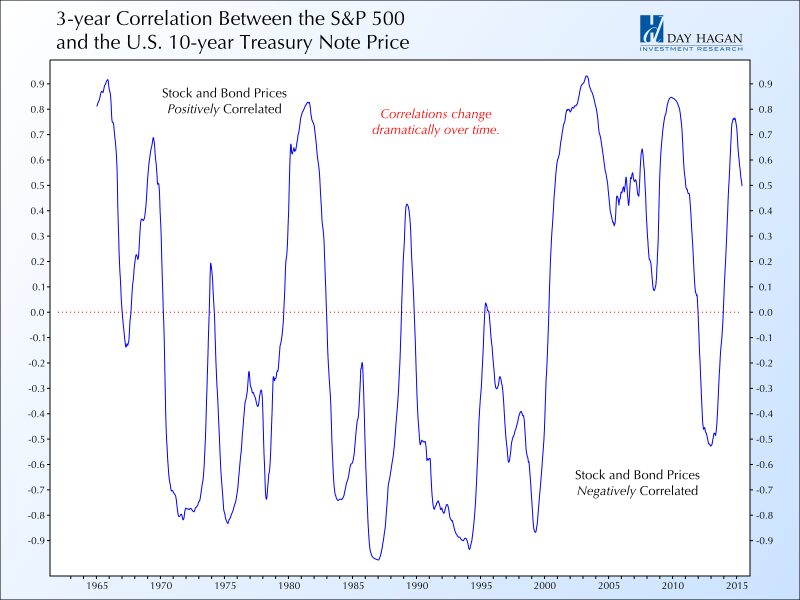

Below is a chart of the rolling 3-year correlation between stock prices and bond prices, with data going back to 1963. As you can see, the correlation changes dramatically from an almost perfectly positive correlation to an almost perfectly negative correlation. But in the Robo-Advisor’s world, the correlation is viewed as always nearly perfectly-positive. When the relationship between stocks and bonds doesn’t behave that way, then the whole MPT, CAPM and Robo-Portfolio allocation system breaks down.

Bottom Line: MPT-based portfolios are flawed because they are based on assumptions that have proven to be untrue and non-factual. The markets just don’t work like MPT theorists thought they would. MPT-based portfolios will only work if markets behave rationally and efficiently, correlations (beta) remain stable (they don’t) and asset classes move in the relative directions that are modeled in and expected (they won’t).

Well, the reality is that Robo-Advisors have been around for decades. It is only now that the marketing has gotten slicker and more pervasive. My guess is that the following will occur:

- People have already forgotten that equities experience Bear markets. Once we get the next Bear market, investors will realize that Robo-Portfolios don’t provide the services that a true high-net-worth investor is seeking.

- Keep in mind that the basic element of risk management that a Robo-Adviser uses is diversification. Know that with a Robo-Advisor, your investment will be based primarily on your age (or time until retirement), and that based on that calculation, you will have the same amount of money invested in stocks whether the Price/Earnings ratio is 8 or 80.

If you want to own everything all the time and don’t care about managing the risks in your portfolio, then Robo-Advisors may be for you.

*The Standard and Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine what is appropriate for you, consult a qualified professional.

No strategy assures success or protects against loss.

Advisory services offered through CWM, LLC a Registered Investment Advisor